Credit unions face growing financial pressures as the holiday season approaches due to rising loan delinquencies and charge-offs. The latest data from the National Credit Union Administration (NCUA) for Q2 2024 highlights concerning trends: members are experiencing increased financial strain, which is driving up loan servicing costs for credit unions.

Key Insights from the NCUA's Q2 2024 Report

The NCUA’s report presents several key data points:

- Delinquency rate: 84 basis points, up 21 points from Q2 2023.

- Net charge-off ratio: 0.79%, an increase of 26 points year-over-year.

This rise in delinquencies and charge-offs places additional pressure on credit unions, particularly when managing the costs associated with servicing delinquent loans. As NCUA Chairman Todd Harper stated, “Notably, an increasing segment of credit union membership continues to experience financial strain as evidenced by a steady increase in the loan delinquency rate, charge-offs, and borrowing using the NCUA’s payday alternative loan product.”

Understanding the Rising Cost of Loan Servicing

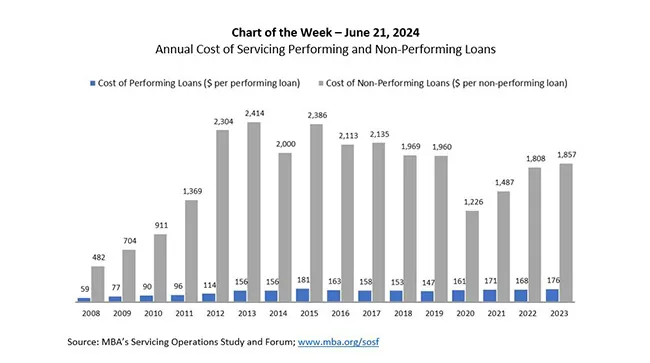

A deeper look at the Mortgage Bankers Association’s (MBA) Servicing Operations Study and Forum reveals how loan servicing costs have shifted in recent years. While fully-loaded servicing costs remained flat at an average of $237 per loan in 2023, the real story lies in the distinction between performing and non-performing loans.

- Performing Loans: Servicing costs increased to $176 per loan in 2023, up from $168 per loan in 2022, driven by statements, billings, quality assurance, and corporate compliance.

- Non-Performing Loans: The average servicing cost rose to $1,857 per loan in 2023, up from $1,808 in the prior year. This increase is due to the division of higher base servicing costs across fewer non-performing loans and a general rise in non-default-related expenses.

The rise in servicing costs for non-performing loans marks the third consecutive year of increases. Despite a decrease in gross default-related costs in 2023, the growing expense highlights the ongoing challenge of managing non-performing loans, even as the number of these loans declines.

Here’s a look at the cost breakdown for servicing performing vs. non-performing loans:

As this chart demonstrates, while overall servicing costs per loan have remained steady year-over-year, the cost of managing non-performing loans continues to climb. This presents a clear need for more efficient processes to manage delinquent accounts for credit unions.

Maximizing Efficiency for Smaller Credit Unions

Due to limited resources, managing delinquencies is especially challenging for smaller credit unions. Lexop’s automation tools help relieve the pressure on small teams by handling routine collections tasks, allowing FTEs to focus on higher-priority activities such as repossessions or complex account management that cannot be automated. By taking care of the “low-hanging fruit,” your team can remain efficient and reduce overall costs without needing to hire additional staff.

Prepare for the Holiday Surge: Streamline Collections and Reduce Costs with Lexop

Time is of the essence, especially with the holiday season approaching, when delinquencies tend to increase. According to Deloitte, holiday retail sales are expected to rise between 2.3% to 3.3% this year. While this signals increased spending, it can also mean financial strain for credit union members in the months that follow—leading to more delinquencies.

Implementing an automated solution now not only positions your credit union to manage delinquencies more efficiently but also helps reduce the cost of loan servicing over time. Lexop’s platform can be up and running within just five weeks, ensuring your team is equipped to handle the seasonal surge without being overwhelmed.

In addition to fast implementation, Lexop offers flexible pricing tailored to meet the needs of credit unions of all sizes. Many of our clients have collected more than the entire value of their Lexop contract within the first month of using our software, highlighting the immediate impact automation can have on collections.

By investing in Lexop now, your credit union can get ahead of these rising costs, streamline your collections process, and minimize the impact of delinquencies. Whether you need to prepare for the holiday rush or stabilize your loan servicing costs, Lexop offers a quick and affordable solution to help you succeed. Book a personalized demo today to see how much time and money you could save this holiday season.